Tax & GST Insights for Indian Businesses

Stay updated with the latest GST updates, income tax tips, company compliance requirements, and financial planning advice for businesses across India. Our articles are written in simple language by our experienced tax team at Gadhia Associate, Junagadh.

24 July 2026

GOODS AND SERVICE TAX

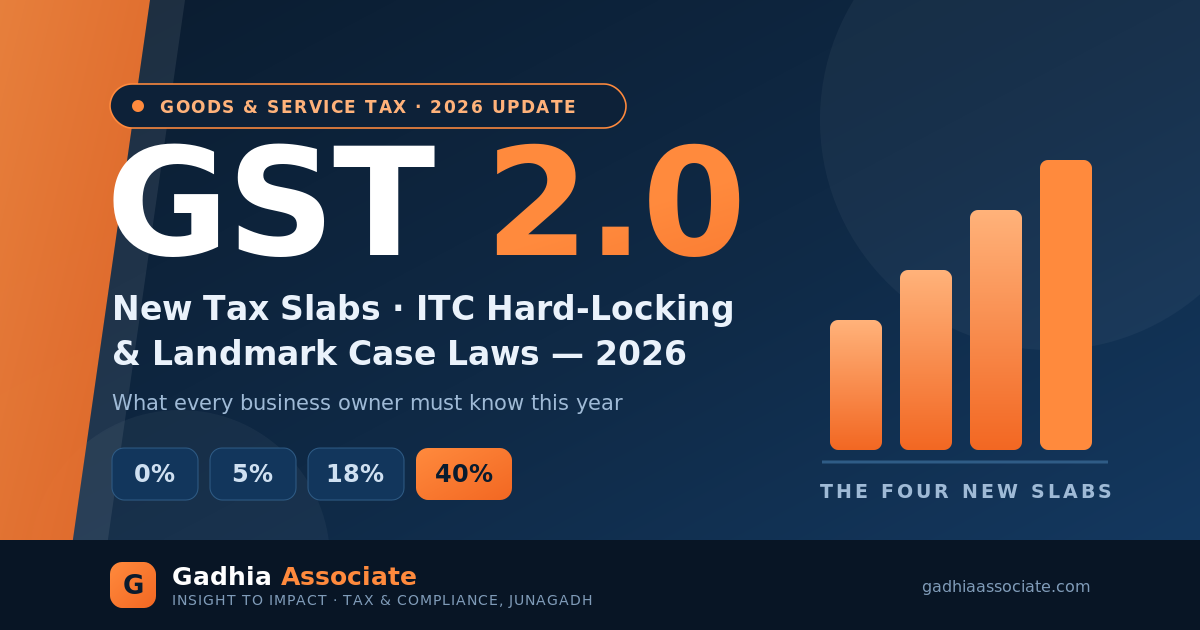

GST 2.0 in 2026: New Tax Slabs, ITC Hard-Locking and Landmark Case Laws Every Business Owner Must Know

67 Views

Read More

14 July 2026

COMPANY AND STARTUP

Your Business May Now Count as an MSME: What the New April 2025 Limits Mean for You

66 Views

Read More

14 July 2026

INCOME TAX

Sending Money Abroad in 2026? The New 2% TCS Rule You Should Know Before You Transfer

72 Views

Read More

11 July 2026

COMPANY AND STARTUP

Section 8 Company or Trust: Which Structure Should You Choose for Your Hospital?

84 Views

Read More

11 July 2026

GOODS AND SERVICE TAX

ISD Registration Under GST: Why It's No Longer Optional for Multi-Branch Businesses in 2026

83 Views

Read More

6 July 2026

INCOME TAX

Your Crypto Exchange Is Now Talking to the Income Tax Department: What Changes From April 2026

86 Views

Read More

6 July 2026

COMPANY AND STARTUP

Your Payroll Just Got More Expensive: What the New Labour Codes Mean for Gujarat Employers

70 Views

Read More

1 July 2026

INCOME TAX

Paid an MSME Vendor Late? Here's What Section 43B(h) Costs You This Tax Audit Season

72 Views

Read More

1 July 2026

FOREIGN EXCHANGE MANAGEMENT ACT - FEMA

FEMA Just Widened Who Can Invest in Your Company - Here's What Changed in June 2026

111 Views

Read More